Political risk and economic uncertainty are now viewed as the leading barriers to growth in the energy industry in the Middle East, according to DNV’s Energy Industry Insights survey. What are companies in the region doing to address this risk to growth?

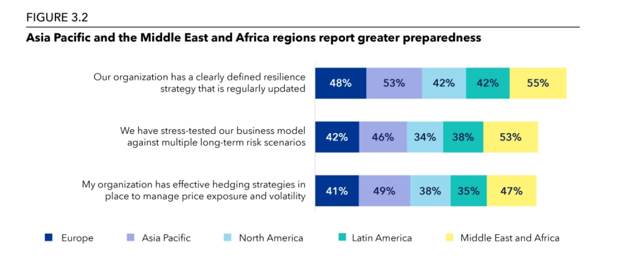

Zschommler: According to the latest DNV Energy Industry Insights 2026 special report, energy companies in the Middle East are responding to political and economic uncertainty by strengthening their resilience. In the Middle East and Africa, 53% of energy leaders report that they are stress-testing their business models against multiple long-term risk scenarios. This indicates a more structured approach to managing uncertainty.

The region demonstrates greater preparedness for risk compared to other parts of the world. Many organisations are establishing resilience strategies and using hedging mechanisms to manage price volatility. Notably, 55% of energy leaders state that they have a clearly defined and regularly updated resilience strategy, while 47% have implemented hedging measures. These findings suggest that, although significant steps are being taken to address risk, preparedness is still evolving.

National oil companies in the Gulf region are increasingly positioning themselves as integrated energy companies. How different will these organisations look in 2040 compared with today?

Zschommler: Gulf national oil companies are expanding their portfolios beyond upstream oil and gas. They are increasing investments in downstream activities and petrochemicals, while also adding renewables and other low-carbon energy sources. This reflects a broader shift in energy and product mix, moving beyond traditional hydrocarbons and including portfolios of fuels, petrochemicals and electricity. At the same time, they are growing their presence internationally, with more investments outside their domestic markets, including in the US, Europe and Asia. Overall, this indicates a move toward more diversified, globally active energy businesses that operate across multiple geographies and parts of the value chain.

Oil and gas demand growth is increasingly driven by Asian markets. What are the practical implications of this for producers in the Gulf region?

Zschommler: Asian-driven demand growth largely aligns with the existing strengths of Gulf producers. They al-ready have strong, long-standing trade relationships with key customers across Asia. This gives them a solid base to build on, allowing them to expand supply and serve growing demand in markets where they are already well positioned. In practical terms, this means Gulf producers can continue to deepen commercial ties and increase volumes to these buyers, reinforcing their role as reliable and trusted suppliers as demand shifts east.

However, this advantage is not without constraints. Ongoing instability in the Strait of Hormuz creates a short-term barrier, as it directly affects the main export route to Asian markets. This introduces uncertainty around supply reliability and can limit the ability to fully respond to demand growth. As a result, how effectively Gulf producers can leverage this opportunity in the near term will depend on how the situation in Hormuz evolves. A resolution to the current instability will be critical in enabling Gulf producers to immediately capitalise on Asian demand growth in a more consistent way.

DNV forecasts that, by 2040, MENA will likely supply 16% of global hydrogen production for energy purposes. Can you outline what needs to happen in terms of infrastructure and regu-lation in the region to ensure this market grows as forecast?

Zschommler: To achieve that level of supply, a few practical enablers need to be in place across both infrastructure and regulation. On the infrastructure side, scaling production is the first require-ment. Gulf producers will need to invest in renewable electricity to support green hydrogen, while also building out CCS capacity to enable blue hydrogen. Both pathways are likely to be needed to reach scale.

In parallel, export infrastructure will need to develop. Given the long-distance export routes heading both east and west for any Middle East export project, hydrogen is unlikely to be traded in its pure form by pipelines. So, conversion into carriers such as ammonia, and potentially methanol or fertiliser products, will be important. This allows large volumes of hydrogen to be transported more easily. Export routes will therefore need to include conversion facilities, as well as port and shipping infra-structure to enable international trade.

On the regulatory side, MENA governments need to move quickly from big ambitions and announcements about hydrogen to putting appropriate rules and structures in place. The urgency is clear from DNV’s own data—delays and reversals in hydrogen policy worldwide have already led DNV to cut its forecast for clean hydrogen by 45% since 2022.

The regulatory work needed maps directly onto the three value-chain stages: production needs car-bon intensity rules and certification schemes; transport needs hydrogen-specific safety and pipeline codes; and export needs Guarantees of Origin, bilateral trade agreements and port regulations. These complete regulations do not yet exist across MENA today, and their absence is

arguably as large a constraint on the 16% forecast as the infrastructure gaps themselves.

You report that CCS has become a central element of MENA’s long-term decarbonisation strategy. What advantages does the Gulf region have over other parts of the world in terms of developing CCS infrastructure?

Zschommler: MENA is well positioned to expand CCS, supported by decades of oil and gas activity that has built a strong and mature energy infrastructure and knowledge base. Extensive pipeline networks, deep subsurface expertise and well-mapped geological formations provide a solid foundation for developing large-scale CO2 transport and storage systems. These factors position the region well compared to others that may not have the same level of existing infrastructure or subsurface experience. Vertically integrated NOCs simplify project setup and decision-making. Major industrial hubs along the Gulf and North African coasts further concentrate emissions, thereby creating practical early opportunities for CCS cluster deployment. Given the significant investments required for large-scale CCS developments, Middle East operators are well positioned, with strong financial capacity to support such projects. Although additional investment and regulatory frameworks will be essential, the existing infrastructure offers a credible platform for accelerating future CCS growth across the region.

DNV forecasts that variable renewable electricity generation will grow 14-fold by 2040 in MENA. What does this shift mean for the region’s long-term reliance on fossil fuels?

Zschommler: While a 14-fold increase in renewable electricity marks a significant shift in MENA’s power system, it does not translate into an immediate decline of fossil fuel dependence. The main reason is that renewable growth does not keep pace with rising electricity demand in the medium term, delaying the decline of fossil fuel use until around 2040. As a result, fossil fuels will continue to play a critical role in the medium term. The displacement of fossil-fired generation is delayed until around 2040, when renewable generation begins to outpace demand growth and a clearer transition point emerges. Over the longer term, however, this rapid renewable expansion gradually shifts the direction of the power system. It lowers the relative role of fossil fuels in electricity generation, with non-fossil sources projected to dominate by mid-century. In practical terms, this means MENA is not moving away from fossil fuels overnight but transitioning gradually from a system where fossil fuels underpin both domestic consumption and exports to one where renewables increasingly meet power needs, while hydrocarbons remain part of the broader energy mix for longer.

If you look at the current landscape today, what is one key risk and one opportunity that de-serve more focus right now?

Zschommler: In the current landscape, geopolitical risk is understandably front of mind and contin-ues to dominate attention. Ongoing tensions are directly affecting supply chains, trade routes and overall market stability, making it the most visible and immediate risk across the sector.

Alongside this, cybersecurity is a risk that deserves more focused attention. DNV’s research identifies cybersecurity as a leading concern, with around two-thirds of energy professionals viewing it as the greatest current risk to their business. On the opportunity side, this same shift points to a clear area for action. DNV’s research emphasises the need to strengthen resilience in increasingly digital and interconnected energy systems, including through cybersecurity risk assessment and assurance.

In practical terms, while geopolitical developments remain the most visible risk, cybersecurity stands out as an area where more focus can translate into stronger operational resilience and better preparedness for a more digital energy system.