Slumping liquids production, energy import dependency, increased gas venting and financial challenges are finally forcing the Mexican authorities to prioritise the country’s substantial unconventional deposits.

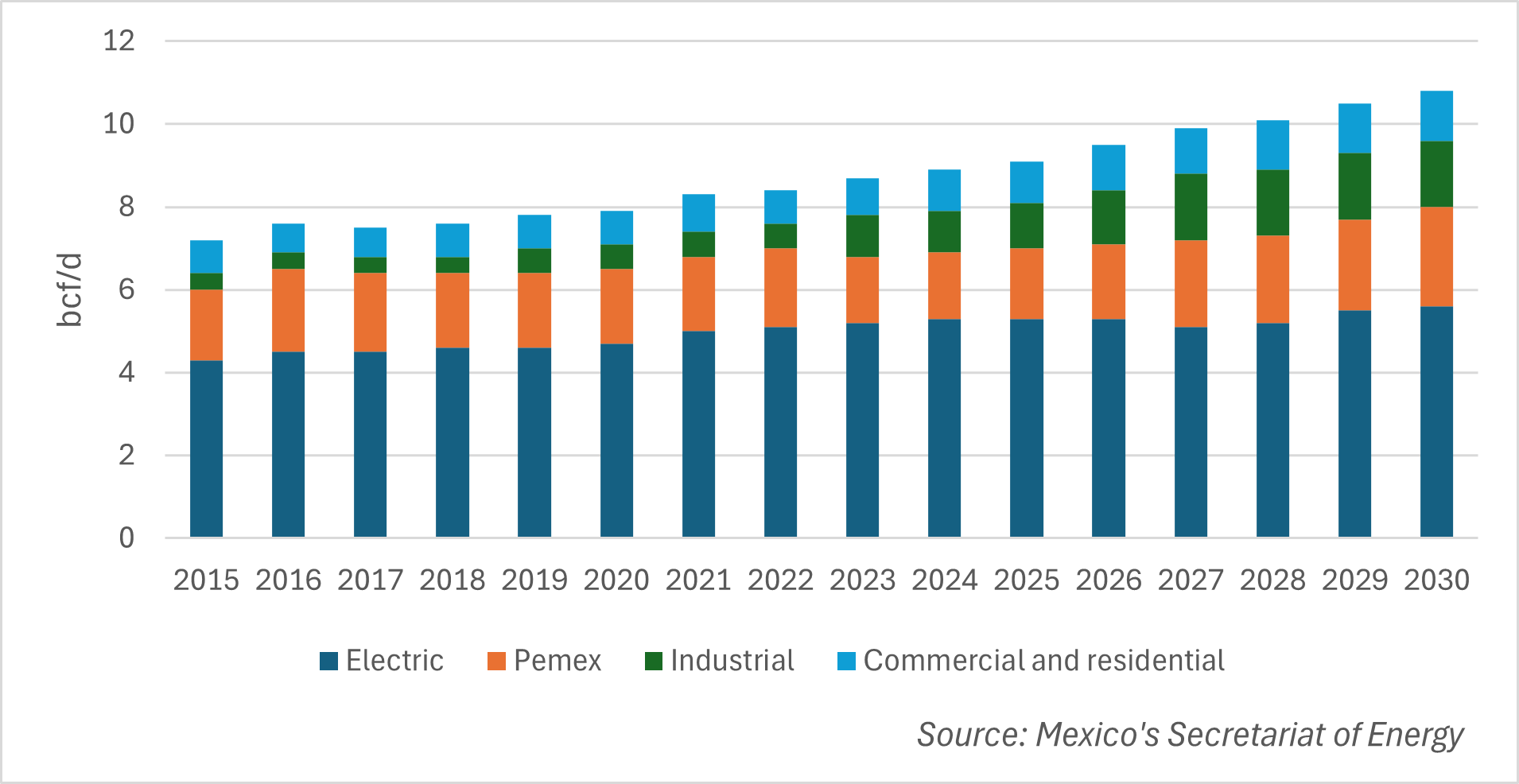

Today, around 75% of Mexico’s gas supply is imported from the US. The government also expects domestic consumption to rise from 9.5bcf/d this year to 10.8bcf/d by the end of the decade, increasing the financial and energy security burden unless local production can be revived.

Mexico’s gas output has declined structurally over the past decade, as NOC Pemex prioritised oil-focused exploration and production, leaving gas development largely underinvested.

Mexican crude production as well as reserves nevertheless fell to their lowest levels in 35 years last year. NOC Pemex averaged 1.635m b/d in 2025, a 7% fall on levels posted in 2024. The company also exported just 581,000b/d, a 27.9% decrease on 2024 and its lowest on record.

“Mexico has experienced structural production decline over the past two decades, driven primarily by the natural decline of Pemex's legacy assets—including Cantarell, Ku, Maloob and Zaap. Exploration has not yielded significant new discoveries in recent years, and current strategy remains focused on enhanced recovery from mature fields and the incremental development of smaller finds.

Pemex is hardly making best use of its gas either. Between March and April, the NOC vented an average of 618mcf/d of gas, the equivalent of 15.7% of total production in Q1 2026, and an increase of 272mcf/d over the same period last year. This was against the backdrop of growing dependence on US imports.

Mexican venting is mostly the result of lack of gas infrastructure and the NOC’s focus on oil recovery (particularly gas handling at the Ixachi field in the Northern Land Region and Bakte field in the Southern Land Region). Pemex is aware of the problem at least and said it would work with the government to put together an action plan to tackle its methane emissions. These rose by 51.2% in Q1 2026 year-on-year.

Changing course

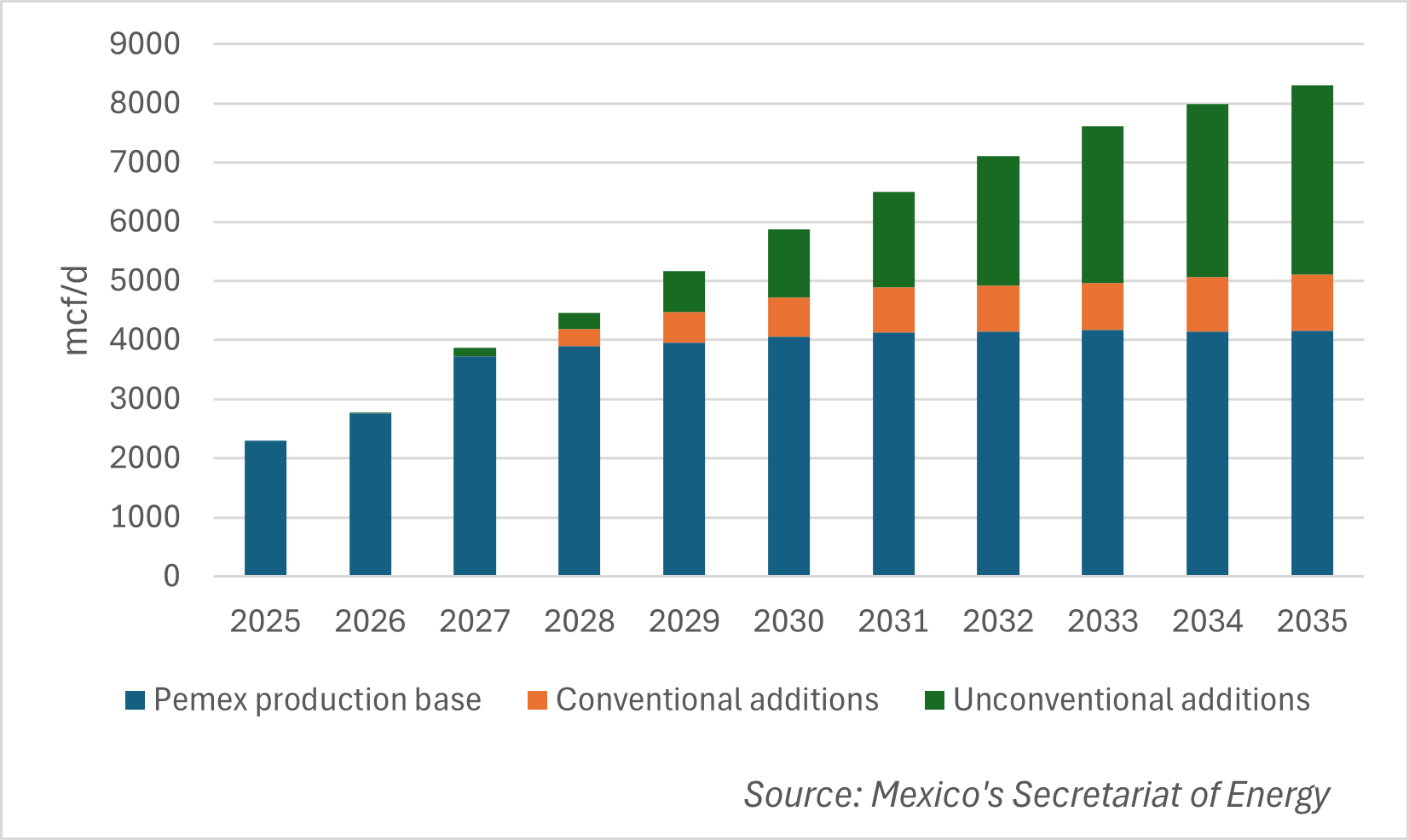

Faced with such dire numbers, in April the Mexican government published its latest energy strategy plan. Moving away from the policy of her predecessor, Andres Manuel Lopez Obrador, Mexican President Claudia Sheinbaum is instead focusing on the country’s untapped unconventional reserves. In total, the government estimates conventional gas reserves at 83,138bcf and unconventional gas reserves at 141,494bcf. If fully developed, the authorities project an additional 3.196bcf/d of gas production by 2035.

“Mexico has sizeable unconventional shale resources, particularly in the Burgos Basin, which could materially reduce import dependence over time if developed successfully” Aamir, Welligence

“Mexico has sizeable unconventional shale resources, particularly in the Burgos Basin, which could materially reduce import dependence over time if developed successfully,” said Shail Aamir, a senior analyst at upstream researcher Welligence Energy Analytics. “The Burgos Basin sits in a region where over 45% of aquifers are already overexploited. [Therefore,] a credible water management framework would need to be established.”

Pemex will likely need private-sector partners to share the capital intensity of these projects, as well as experienced unconventional operators capable of bringing the technology and know-how required to accelerate the path to efficiency. Without this combination, the timeline to meaningful unconventional production will likely be extended substantially.

Developing unconventional resources at scale requires significant capital, specialised technology and operational expertise that Pemex lacks. Consultancy Wood Mackenzie analysts noted that operators in the US spent two decades refining the technology, techniques and workflows that underpin today's efficient shale development; Argentina's Vaca Muerta has followed a similar learning curve.

Despite Pemex cutting its debt to $79b in Q1 2026, its lowest level since 2014, the company remains heavily indebted, and large-scale funding will be challenging. Shortly after the NOC’s latest results were published, it was also revealed that the firm’s CEO, Victor Rodriguez, would be leaving the top job and replaced by CFO Juan Carlos Carpio.

“Security concerns tied to organised crime, limited fracking expertise and infrastructure, and restrictions on foreign private investment make large-scale development difficult,” added Adrian Calcaneo, vice president of energy and feedstocks at OPIS, a Dow Jones company. Mexico’s shale regions also require major new infrastructure—including pipelines, water systems and fracking logistics—making development extremely expensive.

The most realistic path will involve reopening the sector to private and foreign companies that can provide the capital, technology and expertise Mexico lacks. Without broader private participation, large-scale shale development will remain difficult.

Time for greater collaboration?

“The immediate problem is that the current private investment model arguably presents a structural deterrent. Mixed contracts require Pemex to maintain at least 40% participation, and it remains uncertain whether Mexico can offer attractive enough terms to international firms whose expertise would be needed,” Aamir noted.

Showcasing the attempt to attract private participants, Pemex has announced ten new mixed contracts this year, designed to bring partner investment into specific projects tied largely to mature asset production. The NOC has also been in dialogue with Brazilian state oil and gas firm Petrobras to help develop Mexico’s offshore deepwater acreage.

“A partnership with a state-controlled Latin American company from a friendly government may be easier for Mexico’s government to justify than reopening the sector to Western private oil firms,” stressed Calcaneo. Petrobras also brings valuable offshore expertise, particularly in ultra-deepwater drilling. However, Mexico’s deepwater projects are expensive, high-risk and require major long-term investment.

Pemex is only now entering its first deepwater development at Trion, this time in partnership with Australian firm Woodside Energy. Woodmac points out that a collaboration with Petrobras would give Pemex access to proven deepwater capabilities and could facilitate the unlocking of nearby discoveries—including Maximino, Nobilis, Exploratus and Cratos—that stand to benefit from the infrastructure established through Trion. Any formal partnership would likely follow a structure similar to the joint venture framework approved last year, though specific terms would depend on the assets in scope.

Expanding the footprint

Meanwhile, Mexico’s richest man, Carlos Slim, is quietly mopping up acreage and strengthening his claim to the country’s oil and gas sector. In early May, Grupo Carso via a subsidiary took an extra 5% stake in the offshore Zama discovery from UK-based Harbour Energy. The field holds an estimated 600m–800m boe of recoverable reserves, making it one of the largest offshore Mexican discoveries in decades. After approval, Grupo Carso will hold a 17.84% stake in the field, Harbour Energy with 27.26%, Talos Energy with 4.47% and Pemex the largest with 50.43%.

In early May, Grupo Carso also finalised the acquisition of Fieldwood, an operating subsidiary of Russian firm Lukoil. If approved, the deal would give Slim access to Area 4, a licence that includes the promising shallow-water Ichalkil and Pokoch deposits in southeastern Mexico.

Grupo Carso, one of the largest private producers in the country, previously signed an agreement with Pemex to drill the onshore Ixachi field and is reviewing potentially developing the Lakach deepwater field. If the project gets the green light, it would become Mexico’s first ultra-deepwater project under development. Lakach lies off the coast of Veracruz and is estimated to hold approximately 900bcf in gas reserves.

While these private ventures could eventually add to domestic production, at least for the foreseeable future Mexico’s oil and gas output looks unlikely to rebound markedly. For the remainder of 2026, the outlook appears challenging for both Pemex and Mexico overall.

Maintaining current production levels will be difficult without a meaningful increase in investment, drilling or private-sector participation. Production is therefore more likely to remain flat-to-declining rather than show meaningful growth, particularly as mature offshore fields continue to decline and new developments struggle to ramp up quickly enough.